|

Positive Displacement Pumps Industry Data Book Covers Rotary Pumps and Reciprocating Pumps Markets. The economic value generated by the positive displacement pump industry was estimated at approximately USD 18.35 billion in 2022. The demand from various industries such as oil & gas, chemicals, pharmaceuticals, and water treatment is driving this market’s growth. Access the Global Positive Displacement Pumps Industry Data Book from 2023 to 2030, compiled with details by Grand View Research Rotary Pump Market Growth & Trends The global rotary pumps market size was valued USD 10.42 billion in 2022, registering a CAGR of 4.5% from 2023 to 2030, according to a new report by Grand View Research, Inc. The rising demand for fluid handling across diverse industries like oil & gas, chemicals, and wastewater treatment has emerged as the primary driving force behind the market growth. Rotary pumps are gaining prominence due to their versatility in managing a wide range of fluids with varying viscosities, making them a preferred choice. The market is significantly shaped by the expansion of end-use industries, such as oil & gas, food processing, and chemical processing industries. In addition, for oil & gas and food processing industries, it is essential to control the process variables, such as discharge rate & pressure of the fluid. This kind of process control can be easily done with the help of rotary pumps, as they are known for their reliability, versatility, and ability to handle a wide range of fluids. In the oil & gas industry, the American Petroleum Institute (API) has set up standards for various equipment for their use in different industries, including pumps. API Standard 676 covers standards and guidelines for positive displacement rotary pumps. Furthermore, the Hydraulic Institute provides standards related to rotary pumps in the pump industry. It covers standards regarding pump design, testing, installation, and operation. The market is highly competitive, with a majority of players continuously increasing their R&D expenditure. Key players also undertake other strategies including production expansion, mergers & acquisitions, and new product launches. A few established players benefited from a higher scale of production in terms of cost advantage. Manufacturers have been exploring opportunities to develop IoT-based digitalized pumps to control flow rates efficiently. They are designing new energy-efficient products to meet the growing demand for carbon-efficient products. Mature market players are using variable speed drives (VSDs) to further penetrate the market. Order your copy of Free Sample of “Positive Displacement Pumps Industry Data Book - Rotary Pumps and Reciprocating Pumps Market Size, Share, Trends Analysis, And Segment Forecasts, 2023 - 2030” Data Book, published by Grand View Research Reciprocating Pump Market Growth & Trends The global reciprocating pumps market size was valued USD 7.93 billion in 2022, exhibiting a CAGR of 5.0% from 2023 - 2030, according to a new report by Grand View Research, Inc. The expansion of industries such as manufacturing, chemicals, and wastewater treatment is fueling the growth of the reciprocating pumps industry. These pumps play an important role in generating high-pressure fluid. These highly pressurized fluids are then further utilized in hydraulic systems and manufacturing operations. Reciprocating pumps are categorized as positive displacement pumps capable of displacing a consistent volume of fluid at elevated pressures. The reciprocating pumps rely on back-and-forth motion of a piston, plunger, or diaphragm to substantially elevate fluid pressure, facilitating the transfer of fluids from one location to another. In the oil and gas industry, the American Petroleum Institute (API) has set up the standards for various equipment being used, including pumps. API Standard 674 covers standards and guidelines for the positive displacement reciprocating pumps. Furthermore, the Hydraulic Institute, the global authority on pumps and pumping systems, has been providing guidelines & standards regarding the pumps. The ANSI/HI 6.1-6.5 standards cover various aspects of reciprocating power pumps, including their design, operation, and testing. The market is characterized by intense competition, with most companies continuously increasing their investments in research and development. Moreover, key players follow strategies such as facility expansion, mergers, acquisitions, and introduction of new products in the market. The future market is being shaped by changing demands in end-use industries, such as a growing emphasis on energy efficiency and sustainability. Leading market participants are designing pumps that are more energy-efficient and have a lower carbon footprint. These innovative pumps are equipped with variable frequency drives (VFDs) to enhance pump speed and flow control capabilities. Go through the table of content of Positive Displacement Pumps Industry Data Book to get a better understanding of the Coverage & Scope of the study. Competitive Landscape Key players operating in the Positive Displacement Pumps Industry are – • Ingersoll Rand SPX Flow • Alfa Laval • Viking Pump, Inc. • Grundfos • Schlumberger Limited • KSB Group • Sulzer Ltd Global positive displacement pump sector database is a collection of market sizing information & forecasts, competitive benchmarking analyses, macro-environmental analyses, and regulatory & technological framework studies. Within the purview of the database, such information is systematically analyzed and provided in the form of outlook reports and summary presentations on individual areas of research.

0 Comments

Interior Construction Materials Industry | Exploring The Vast World From Floors To Ceilings1/26/2024 Global interior construction materials sector data book is a collection of market sizing information & forecasts, trade data, pricing intelligence, competitive benchmarking analyses, macro-environmental analyses, and regulatory & technological framework studies. Within the purview of the database, such information is systematically analyzed and provided in the form of outlook reports (1 detailed sectoral outlook report) and summary presentations on individual areas of research.

The economic value generated by the interior construction materials industry was estimated at approximately USD 578.06 billion in 2022. This economic output is an amalgamation of businesses that are involved in the manufacturing of interior construction materials, distribution & supply, and application of interior construction materials. Ceiling Tiles Market Growth & Trends The global ceiling tiles market size was valued USD 6.82 billion in 2022, registering a CAGR of 9.4% over the forecast period. Ceiling tiles are used in a variety of residential and non-residential applications. The non-residential application of ceiling tiles dominated the application segment due to its high adoption in institutional buildings, office complexes, and healthcare facilities worldwide. The market growth is attributed to the rising usage of sustainable, eco-friendly, and innovative building material solutions owing to a rise in disposable incomes and changing consumer behavior towards the aesthetics of home and office buildings. U.S. has dominated the ceiling tiles market and accounted for a revenue share of 28.1% in 2022, followed by China, Germany, and the UK. The market for ceiling tiles in the U.S. is driven by changing consumer behavior towards the adoption of sustainable building solutions coupled with rising demand for soundproof and decorative interior construction materials in non-residential applications. Insulation Market Analysis And Forecast The global ceiling tiles market size was valued USD 61.36 billion in 2022, registering a CAGR of 6.6% over the forecast periodRising consumer awareness about energy conservation is likely to remain a crucial driving factor for the global insulation market. Favorable regulations in the majority of regions are also expected to have a positive impact on market growth. Additionally, increased infrastructure spending in the emerging markets of Asia Pacific and Latin America is expected to propel the insulation market's growth. The high rate of industrialization, along with rapid urbanization in the emerging markets of China and India, as well as Japan, Malaysia, Thailand, and Indonesia, have driven the need for better infrastructure. Increasing construction spending to improve residential, public, and industrial infrastructure in the region, coupled with the increasing adoption of energy conservation initiatives, is expected to drive the demand for insulation over the forecast period. Flooring Market Growth & Trends The global ceiling tiles market size was valued USD 266.47 billion in 2022, registering a CAGR of 5.2% over the forecast periodThe flooring market is growing at a significant rate owing to a rise in infrastructural and residential development as a result of the growing population across the globe. In addition, rising disposable incomes have increased investment in comfortable residential buildings, resulting in the use of high-end building materials in construction. These factors are expected to increase the demand for flooring over the coming years. China has dominated the flooring market and accounted for a revenue share of 16.5% in 2022, followed by the U.S. and India. The market growth in the major countries is attributed to the increasing investment in affordable housing, smart city construction, upgradation, and construction of infrastructure. Order your copy of Free Sample of “Interior Construction Materials Industry Data Book - Interior Construction Materials, Flooring, Insulation, Ceiling Tiles, Windows and Doors Market Size, Share, Trends Analysis, And Segment Forecasts, 2023 - 2030” Data Book, published by Grand View Research Windows and Doors Market Analysis And Forecast The global windows and doors market size was valued USD 243.40 billion in 2022, registering a CAGR of 9.4% over the forecast period. The windows and doors market is expected to grow at a faster pace over the coming years. This is due to the rising construction and renovation activities across the globe. In addition, growing disposable incomes, a rising population, increasing remodeling activities, and government initiatives for the construction of affordable housing solutions are expected to fuel the growth of the windows and doors market in the coming years. China has led the windows and doors market and it is expected to expand at a significant CAGR over the coming years. Factors such as the rising population, rapid urbanization, commercialization, and growing investments in the construction of houses with smart windows and doors technology are expected to boost the growth of the market in the country. Competitive Landscape Key players operating in the Interior Construction Materials Industry are – • Mohawk Industries, Inc. • GAF Materials Corporation • AWI Licensing LLC • Tarkett, S.A. • ROCKWOOL International A/S • Burke Flooring Products, Inc. • Pella Corporation • Huntsman International LLC • SAS International • Milgard Manufacturing, LLC • DuPont • Saint-Gobain Gyproc • Shaw Industries, Inc. • Kömmerling • Owens Corning • Knauf Digital GmbH • Ply Gem Residential Solutions • Forbo Flooring • HIL Limited • BASF Polyurethanes GmbH Global long steel products sector database is a collection of market sizing information & forecasts, trade data, pricing intelligence, competitive benchmarking analyses, macro-environmental analyses, and regulatory & technological framework studies. Within the purview of the database, such information is systematically analyzed and provided in the form of outlook reports (1 detailed sectoral outlook report) and summary presentations on individual areas of research along with an agricultural statistics e-book.

Steel is a vital industry for global economic growth and long steel products play a crucial role in the development of infrastructure across the globe. It is a key raw material used in producing long products for building & construction and various manufacturing activities. As per the World Steel Association, the total value contribution by the steel industry is USD 2.9 trillion, which is equivalent to 3.8% of global GDP. Steel Rebar Market Growth & Trends The global steel rebar market size was valued USD 258.44 billion in 2022, according to a new report by Grand View Research, Inc., expanding at a CAGR of 2.9% from 2023 to 2030. The construction segment dominated the steel rebar market, with applications such as construction, infrastructure, and industrial purposes. Asia Pacific accounted for more than half of global steel rebar demand, owing to the easy availability of raw materials and investments in construction activities. China ranked among the top producers and consumers of steel rebar globally. India follows suit after China, as the second largest consumer of steel rebar. The demand in these countries is primarily driven by investments in construction and infrastructure through government-aided policies to boost development in the region. Wire Rod Market Growth & Trends The global wire rod market size was valued USD 186.00 billion in 2022, according to a new report by Grand View Research, Inc. The market is expected to expand at a CAGR of 4.6% from 2023 to 2030. Wire rods are manufactured by drawing hot metals through shafts to develop wires with reduced diameters. Wire rods represent the most ductile form of long steel products owing to their high ductility and easy availability in different diameters. They are widely used in construction and fencing applications. Increasing investments in infrastructure development projects and flourishing construction and automotive industries worldwide fuel the global consumption of wire rods. The demand for wire rods is closely linked to the construction sector, which tends to be cyclical and can be affected by factors such as interest rates, government policies, and economic growth. Growing infrastructure investments in the North American region are anticipated to benefit the growth of the market. For instance, under the Infrastructure Development Act passed by the U.S. government, the authorities are estimating that California is likely to receive USD 14.00 billion for rebuilding infrastructures, including water supply, bridges, roads, and communication. Similar investments were announced for other states in the U.S. Steel Sections Market Growth & Trends The global steel sections market size was valued USD 123.10 billion in 2022, registering a CAGR of 4.5%, according to a new report by Grand View Research, Inc. Steel sections are commonly used in the construction industry, they also have a significant role in the automotive industry. The demand for steel sections in the automotive industry is growing due to several factors, including safety requirements, lightweight, cost-effectiveness, design flexibility, durability, and corrosion resistance. The non-residential construction segment held the largest revenue share of over 54.0% of the global market in 2022. Growth in the non-residential construction industry, driven by urbanization, infrastructure development, and economic growth, has increased the demand for steel sections. Asia Pacific dominated the global steel section market and is expected to continue over the forecast period. The stronghold of the region is attributable to the presence of raw material suppliers, manufacturers, and end-users. Asia-based manufacturers are expanding their production to cater not just to domestic customers but to international demand as well. Order your copy of Free Sample of “Long Steel Products Industry Data Book - Steel Rebar, Carbon Steel Pipe Fittings, Steel Pipes & Tubes and Steel Wire Market Size, Share, Trends Analysis, And Segment Forecasts, 2023 - 2030” Data Book, published by Grand View Research Steel Pipes and Tubes Market Growth & Trends The global steel pipes and tubes market size was valued USD 185.47 billion in 2022, according to a new report by Grand View Research, Inc. It is expected to expand at a compound annual growth rate (CAGR) of 3.7% from 2023 to 2030. Increasing oil & gas production owing to the demand from the transportation industry is one of the prominent growth drivers for the market. The oil & gas industry is the major consumer segment for steel pipes & tubes. Asia Pacific emerged as the leading regional market in 2022 and accounted for a revenue share of over 64.7%, owing to the rising product consumption in the region. China, Japan, South Korea, Southeast Asia, and India are the major product consumers in the region owing to the presence of huge manufacturing, petroleum, and petrochemical sectors. The Middle East & Africa are expected to register a growth rate of 1.8% in revenue in the said forecast period. Rising investment in the new oil & gas project is expected to propel the demand for pipes & tubes in the forecast period. Egypt has set its sights on increasing its oil production by 11% in 2023, aiming to reach a daily output of 650,000 barrels compared to the current 587,000 barrels daily. This expansion plan aligns with the commencement of operations in new oil fields and the expansion of existing fields in the Suez Canal region. Competitive Landscape Key players operating in the Long Steel Products Industry are – • ArcelorMittal • AWAJI MATERIA CO., LTD. • Baosteel • Bassi Luigi & C.S.p.A • Bekaert • Delcorte • Erne Fittinga GmbH • Evraz Plc • Gerdau S.A. • Henan Hengxing Science & technology Co., Ltd • Hyundai Steel • JFE Steel Corporation • Jindal Steel & Power Ltd. (JSPL) • JSW Steel Limited • Kobe Steel Limited • Nippon Steel Corporation • NLMK • Nucor • PARKER HANNFIN CORPORATION • Rama Steel Tubes Ltd. • S.S.E. Pipefittings Limited • Steel Authority of India Ltd. (SAIL) • Tata Steel Group • Tianjin Huayuan Metal Wire Products Co.Ltd. • United States Steel • Wuhan Iron & Steel Corporation Global ferroalloys industry data book is a collection of market sizing information & forecasts, trade data, pricing intelligence, competitive benchmarking analyses, macro-environmental analyses, and regulatory & technological framework studies. Within the purview of the database, such information is systematically analyzed and provided in the form of outlook reports (1 detailed sectoral outlook report) and summary presentations on individual areas of research along with an agricultural statistics e-book.

Ferro Manganese Market Analysis & Forecast The global ferro manganese market size was valued at USD 14.2 billion in 2019 and is expected to expand at a compound annual growth rate (CAGR) of 4.0% from 2020 to 2027. The increasing popularity of cast iron cookware is projected to aid market growth over the forecast period. Ferro manganese is widely used as a sulfur counterpart in the production of cast iron. The ability of the product to remove sulfur contaminants by forming manganese sulfide offers a great advantage as it can easily be removed as slag. The cast iron production historically has observed tremendous growth, for instance, global cast iron production has grown from nearly 54 million tons to approximately 96 million tons from 2000 to 2019. The use of cast iron, especially in cookware, has witnessed a steady climb owing to its ability to offer non-sticky, anti-rust, and durable quality utensils. Thus, the rising production of cast iron is projected to remain a key driver for the market over the forecast period. However, with the breakout of the COVID-19 pandemic, the dynamics of the ferro manganese industry evolved rapidly and stronger demand for the product was observed in European countries amid the fear of complete lockdown. Many European suppliers of the product stated the greater stocking of ferro manganese by still mills in the Northern Italy region. Although this trend was short lived as the downstream demand for steel products declined rapidly. As per the stats released by the World Steel Association, the global steel demand is estimated to contract by nearly 6.4% in FY 2020. The downward sentiments in the global steel marketspace are anticipated to affect the growth of the ferro manganese sector over the short-term period. The industry vendors owing to the breakout of COVID-19 are under severe distress as the downstream demand from the steel industry is going toward a negative trajectory. Owing to the falling demand from the steel sector, Vale, which is among the prominent producers of ferro manganese, closed its plant operations in Simoes Filho, Brazil. Many market participants have devised strategies to cut down expenditure by operating at minimal capacities. Access the Global Ferroalloys Industry Data Book from 2023 to 2030, compiled with details by Grand View Research Ferrochrome Market Analysis & Forecast The global ferrochrome market size was valued at USD 16.77 billion in 2018 and is anticipated to grow at a compound annual growth rate (CAGR) of 4.6% from 2019 to 2030. The market is mainly driven by demand from booming stainless steel industry especially in Asia. Stainless steel industry accounts for roughly more than 75% of the FeCr consumption in the globe. China, being the largest stainless steel producer is therefore also the biggest consumer of FeCr. The global stainless steel production is predicted to witness considerable growth over the coming years owing to strong demand from building & construction industry. Stainless steel is largely consumed in building & construction industry due to its aesthetic appearance and corrosion resistance properties. Moreover, a variety of stainless steel products are easily fabricated and therefore, preferred by architects and building contractors. Majority of chromite ore suppliers in these regions are integrated in nature as they are also involved with manufacturing of ferrochrome. Glencore and Samancor Chrome are some of the major players in South Africa that produce ferrochrome by extracting chromite from their own operating mines situated in South Africa. The chromite ore suppliers are concentrated in South Africa, Kazakhstan, India, Turkey, and Zimbabwe, as these countries are host to enormous amount of chromite ore reserves. Industry rivalry in ferrochrome market is quite intensive owing to the presence of several established and integrated companies that are consolidated in South Africa, India, Turkey, and Kazakhstan. China is also among the largest suppliers of the FeCr along with South Africa. However, the suppliers in China is characterized by various small to medium sized players that import chrome ore mainly from South Africa for their FeCr production. Silico Manganese Market Analysis & Forecast The global silico manganese market size was valued at USD 26.74 billion in 2021 and is estimated to expand at a compounded annual growth rate (CAGR) of 6.5% in terms of revenue from 2022 to 2033. Increasing investments in construction activities across the globe are expected to boost the demand for steel, which is anticipated to positively influence the market growth of silico manganese over the forecast period. For instance, In November 2021, Bahrain announced plans to invest USD 30.00 billion for the creation of five new cities on its manmade islands. The project is a part of the government’s efforts to boost its economy post-pandemic. In addition, the governments of different countries across the Middle East & Africa are investing in tourism and hotel development projects. Silico manganese is a type of ferroalloy that is made up of alloys of manganese, silicon, iron, and a small amount of carbon and other elements. It finds application in steel making, where it is used as a deoxidizer, and to increase the manganese content to improve steel strength. Thus, the rising production of steel is expected to drive the demand for the product. Ferrosilicon Market Analysis & Forecast The global ferrosilicon market size was valued at USD 11.25 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 2.5% from 2023 to 2030. Rising demand for ferrosilicon in the steel and cast iron industries is anticipated to contribute to market growth over the forecast period. Ferrosilicon is used as a deoxidizer in the steel industry to prevent the loss of carbon during the production process. As a result, rising investment in the steel industry is anticipated to augment the market growth. For instance, in January 2022, POSCO commenced construction of a new galvanized steel plant in Tangshan, Hebei, China, which is jointly owned by HBIS Group. The USD 600 million plants are anticipated to have an annual production capacity of 900 kilotons and will supply galvanized steel sheets to the automotive industry. Furthermore, due to their long life span and good compressive strength, cast iron pipes are widely used in plumbing applications. Companies involved in cast iron pipe production are expanding their capacity, thereby fueling ferrosilicon consumption. For instance, in December 2021, AMERICAN SpiralWeld Pipe Company, a producer of cast iron pipe, announced its decision to invest USD 40 million to expand its operation in Richland County, U.S. Furthermore, rising investments in China’s construction industry are expected to benefit market growth. For instance, China initiated five major infrastructure projects in the third quarter of 2021, one of them was an investment of USD 4,793 million in the construction of a railway line from Liuzhou to Wuzhou covering a distance of 237.78 kilometers. Such projects are aiding the consumption of steel and related products, thereby, positively influencing market growth over the forecast period. The market is competitive with a presence of a large number of players scattered across different regions. To uphold and expand their presence, market vendors are involved in acquisition activities. For instance, in February 2022, Elkem ASA acquired the remaining 50% stake in the Salten energy recovery plant from Kvitebjørn Energi, thus, taking 100% ownership. This acquisition aims to enable the production of environmental-friendly ferrosilicon grade. Order Free Sample Copy of Ferroalloys Industry Data Book, published by Grand View Research Key players operating in the ferroalloys industry are – • Arcelor Mittal • Brahm Group • China Minmetals Group Co., Ltd. • Elkem ASA • EMCO • Eramet Group • Eurasian Resource Group • Ferroalloys Corporation Limited • Ferroglobe • FINNFJORD AS • Glencore • Gulf Manganese Corporation Limited • IMFA • Jindal Group • Monet Group • NIPPON DENKO CO., LTD • OM Holdings Ltd. • Russian Ferro-Alloys Inc. • S.C. Feral S.R.L • Sabayek • SAIL • SAKURA FERROALLOYS • Samancore Chrome • Shanghai Shenjia Ferroalloys Co. Ltd • SINOGU CHINA • South32 • Steelforce • Tata Steel • TNC Kazhachrome JSC • Vale • VBC Ferroalloys Limited Global heating equipment industry database is a collection of market sizing information & forecasts, competitive benchmarking analyses, macro-environmental analyses, and regulatory & technological framework studies. Within the purview of the database, such information is systematically analyzed and provided in the form of outlook reports and summary presentations on individual areas of research. Heat Pump Market Report Highlights The global heat pump market size is anticipated to reach USD 166.65 billion by 2030, expanding at a CAGR of 9.3% during the forecast period, according to a new report by Grand View Research, Inc. Favorable government policies for energy-efficient solutions and lowered carbon footprint are expected to boost the market growth over the forecast period. In addition, consumer-driven demand for energy-efficient heat pumps to reduce energy consumption and lower operating expenses are expected to benefit the overall market over the forecast period. The emergence of climate and energy as a political priority has spurred an increased interest in heating and energy efficiency gains to be realized within buildings. Increasing disposable income has led to the growing demand for technologically advanced equipment and comfortable housing solutions, which is further projected to boost the demand for heat pumps. These factors are expected to play a vital role in driving the market growth. Governments across the globe are becoming increasingly aware of the risks associated with fossil fuels and are adopting environment-friendly options. Furthermore, initiatives like the federal tax credit for new residential heat pumps in the U.S. was extended until the end of 2022. The California Energy Commission passed a new building energy code in August 2021, which encouraged the use of heat pumps for space and water heating in newly constructed buildings. All these aforementioned factors are expected to boost the demand for heat pumps in the coming years. Access the Global Heating Equipment Industry Data Book, 2023 to 2030, compiled with details like market sizing information & forecasts, trade data, pricing intelligence, competitive benchmarking, macro-environmental analyses, and regulatory & technological framework studies. Unitary Heaters Market Report Highlights The global unitary heaters market size is anticipated to reach USD 3,122.6 million by 2030, growing at a CAGR of 3.9% during the forecast period, according to a new report by Grand View Research, Inc. Increasing construction spending along with growing demand for highly energy-efficient heating solutions is projected to drive the demand for unitary heaters. Furthermore, favorable government initiatives such as rebates and incentives for the installation of highly energy-efficient unitary heaters are projected to have a positive impact on the market. Unitary heaters are commonly utilized in the commercial sector to address the space heating needs of small complexes or rooms. Unitary heaters have a low starting cost and an easy installation procedure. These reasons are expected to fuel market growth in the coming years. For instance, Warren Technologies provides unitary electric heaters in various sizes, shapes, and configurations that can be field mounted in any brand of air conditioning system. Rising demand for low-noise operations, increasing integration of electric heaters with solar panels, growing use of sensors to adjust the temperature automatically, and elevated efficiency at lower costs are expected to be the major factors driving the demand for unitary heaters in the coming years. For instance, electric unitary heaters are available for installing various types of high-efficiency equipment, including split, packaging, central DX, heat pump, and PTAC systems. Warm Air Furnace Market Report Highlights The global warm air furnaces market size is expected to reach USD 10.8 billion by 2030, growing at a CAGR of 3.2% from 2023 to 2030, according to a new report by Grand View Research, Inc. Increasing construction spending, as well as growing demand for highly energy-efficient heating solutions, are expected to drive demand for warm air furnaces across the globe. Furthermore, favorable government measures such as incentives for the installation of energy-efficient warm air furnaces are expected to benefit the market. The U.S. construction activity increased by over 6% yearly in 2021 and 2022 after a 1.9% drop in 2020. The demand for single-family homes is the main factor driving the rapid residential construction. The strong demand for home remodeling and upgrading is still present because of increased discretionary household spending. A large portion of this growth will come from a significant rise in spending on residential building construction. The demand for warm air furnaces in the residential application segment is expected to be driven by the expanding residential sector in the U.S. Furnaces use heat to circulate hot air using ducts throughout residential spaces due to the presence of drastic temperature changes. Furthermore, in the year 2022, the U.S. Energy Information Administration (EIA) reported that 538,000 of the 911,000 new single-family homes had forced-air furnaces installed. Order your copy of Free Sample of “Heating Equipment Industry Data Book - Heat Pump, Unitary Heaters, Warm Air Furnace and Space Heating Boilers Market Size, Share, Trends Analysis, And Segment Forecasts, 2023 - 2030” Data Book, published by Grand View Research Space Heating Boilers Market Report Highlights The global space heating boilers market size is anticipated to reach USD 35.7 billion by 2030, growing at a CAGR of 3.4% during the forecast period, according to a new report by Grand View Research, Inc. Rapid construction spending coupled with favorable government measures such as the installation of energy-efficient products are expected to benefit the space heating boiler market. For instance, the ENERGY STAR website states that through 2032, federal income tax credits for energy-efficient home upgrades would be offered under the Inflation Reduction Act of 2022. Consumers may successfully migrate to a sustainable energy future by utilizing tax credits and any applicable subsidies, thereby driving market growth. The primary energy consumption in the U.S. accounted for 16% of the primary energy consumed globally in 2021, according to the U.S. Energy Information Administration. Despite having about 4% of the world's population in 2021, the U.S. ranked 10th in the world for primary energy use per person. Due to the methods of sourcing, transportation, and potential for leaks that could increase methane emissions, the use of major energy sources such as natural gas and LP gas has raised environmental concerns. Thus, growing environmental concerns coupled with rising demand for energy-efficient products are expected to drive the demand over the forecast period. Key players operating in the Heating Equipment Industry are – • Lennox International, Inc. • Daikin Industries, Ltd. • Johnson Controls, Inc. • Robert Bosch GmbH • Carrier • Mitsubishi Electric Corporation • Danfoss • LG Electronics, Inc. • Johnson Controls, Inc Electric off-highway equipment industry data book covers electric agriculture equipment, construction equipment, mining equipment market.

Global Electric Off-Highway Equipment Industry databook is a collection of market sizing information & forecasts, competitive benchmarking analyses, macro-environmental analyses, and regulatory & technological framework studies. Within the purview of the database, all such information is systematically analyzed and provided in the form of presentations and detailed outlook reports on individual areas of research. Access the Global Electric Off-Highway Equipment Industry Data Book from 2023 to 2030, compiled with details by Grand View Research Electric Agriculture Equipment Market Insights Growing commercial farming coupled with a labour shortage is a major factor driving the market growth for electric agricultural equipment. The demand for increased crop yield and the hovering threat of food security is other factors supplementing the market growth for electric agricultural equipment in major agricultural economies. The integration of electric propulsion in agricultural mechanisms owing to increased crop yield, decreased production cost, reduction in post-harvest losses, and efficient time management are also favouring the market growth worldwide. The growing traction towards farm mechanization is supporting the uptake of electric technology. Electrical agricultural equipment like tractors, threshers, and other cultivation equipment can aid in numerous farming chores. In order to execute a number of crop production processes, mechanization entails the careful application of inputs by utilizing agricultural equipment, such as power-driven machinery and hand tool, which guarantees a decrease in the labour-intensive tasks associated with various farm activities and refocuses the use of inputs to maximize the potential of available resources. Construction Equipment Market Insights The electric construction equipment market is experiencing growth owing to stringent laws on noise and carbon emissions caused in closed construction and urban area. The increase in noise pollution in the cities has become a potential threat owing to ramping up construction projects. The noise pollution from the equipment, such as loaders, excavators, and motor graders, have prompted municipal corporation in European cities such as Copenhagen, Oslo, Stockholm, and Helsinki to launch initiatives to launch pilot projects for zero-emission construction sites. The city of Helsinki signed the green deal in 2020 to create zero-emission worksites, and the practice will be slowly applied to the whole town. The authorities said that as a result of the initiative, it has chosen to use minimal parameters for procuring all upcoming street infrastructure and outsourced infrastructure projects. By 2025, every city's construction sites are expected to be fossil fuel-free; by 2030, all emissions will be eliminated. Similarly, by 2040 London has also declared its intention to reduce emissions from construction sites to zero. The trend for fast-charging equipment, which has a longer operating duration and is powered by hydrogen fuel, solid-state battery, or lithium-ion battery, is gaining traction while supporting the market growth. Fast-charging batteries are known to withstand higher charging speeds prompting manufacturers to offer battery packs that can be swapped when the battery level is low. Order your copy of the "Electric Off-Highway Equipment Industry Data Book –Market Size, Share, Trends Analysis And Segment Forecasts, 2023 - 2030” Data Book, published by Grand View Research Mining Equipment Market Insights The mining industry has been dependent on diesel for its major operation, such as transportation vehicles, along with operating mining equipment for underground and surface mining. According to International Council on Mining and Metals (ICMM), diesel-powered engines emit 30 to 80 % of emissions in a mining site. With mining concentrated in hostile and harsh terrains with extreme temperatures, the emission emitted contributes to the higher temperature. Using diesel-powered equipment generates more pollutants while producing more noise and heat while incurring higher operational costs. These factors of conventional mining equipment are fueling the adoption of electric mining equipment in the mining industry. Electric mining equipment help in reducing heat in underground mine by increasing ventilation and cooling in the underground mining environment. The ongoing urbanization and industrialization are fueling the demand for natural resources such as oil and minerals. As a result, the global mining industry is flourishing. This, in turn, is expected to boost the demand for electric mining equipment, thereby leading to the growth of the market for this equipment worldwide. Companies operating in the mining equipment market are enhancing their product portfolio by including electric equipment in the lineup to meet the demand for various types of electric mining equipment, such as mineral processing equipment, crushers, surface mining tools, screening equipment, and mining drills & breakers. A range of variants that are either rechargeable batteries, cable-tethered, or use overhead trolley lines make up the most electrified mining equipment. The latter are more common in open-pit mines where using big surface trucks is necessary. Key players operating in the electric off-highway equipment industry are – • Komatsu Ltd • Caterpillar Inc • MaterMacc S.p.A • AGCO Corp. • CLAAS KGaAmbH • Mahindra & Mahindra Ltd. • SDF S.p.A. • J C Bamford Excavators Ltd • AGCO Corp. • CNH Industrial N.V. • Deere & Company • CLAAS KGaAmbH • Escorts Ltd. • International Tractors Ltd. • YanmarCo., Ltd. • KubotaCorp. • Mahindra & Mahindra Ltd. • Tractors and Farm Equipment Ltd. • Caterpillar Inc MaterMacc S.p.A • MaterMacc S.p.A • AB Volvo • Caterpillar Inc • Liebherr Go through the table of content of Industry Data Book to get a better understanding of the Coverage & Scope of the study. About Grand View Research Grand View Research, U.S.-based market research and consulting company, provides syndicated as well as customized research reports and consulting services. Registered in California and headquartered in San Francisco, the company comprises over 425 analysts and consultants, adding more than 1200 market research reports to its vast database each year. These reports offer in-depth analysis on 46 industries across 25 major countries worldwide. With the help of an interactive market intelligence platform, Grand View Research helps Fortune 500 companies and renowned academic institutes understand the global and regional business environment and gauge the opportunities that lie ahead. Global filtration membrane sector database is a collection of market sizing information & forecasts, trade data, pricing intelligence, competitive benchmarking analyses, macro-environmental analyses, and regulatory & technological framework studies. Within the purview of the database, such information is systematically analyzed and provided in the form of outlook reports (1 detailed sectoral outlook report) and summary presentations on individual areas of research.

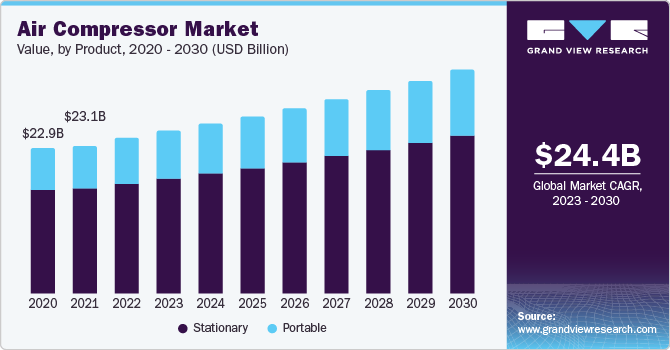

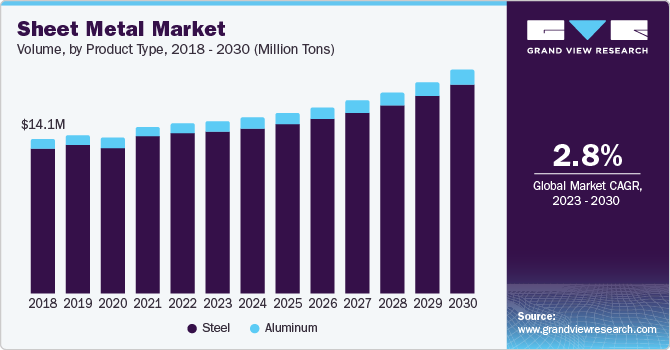

Spiral Membranes Market Report Highlights The global spiral membranes market size was reached to USD 7,659.5 million in 2022 registering a CAGR of 12.1% from 2023 to 2030, according to a new report by Grand View Research, Inc. • Polyamide accounted for the largest market share of over 41% in 2019 and is projected to expand further at a steady CAGR from 2020 to 2027 owing to easy availability and low cost of these polymers • Reverse osmosis was the largest technology segment in 2019 and accounted for more than 40% of the global market share. The segment is estimated to retain its leading position throughout the forecast period as reverse osmosis technology exhibits a considerably higher recovery rate than the traditional thermal desalination processes • The water & wastewater treatment end-use segment is projected to account for the maximum revenue share by 2027 • Growing focus on maximizing the recycling of municipal and industrial wastewater discharge is likely to benefit the segment growth • Asia Pacific is projected to be the fastest-growing regional market from 2020 to 2027 owing to the rapid industrialization • China led the APAC regional market in 2019 and is estimated to register a CAGR of 13.2% from 2020 to 2027 mainly due to the implementation of stringent regulations regarding environmental safety. Access the Global Filtration Membrane Industry Data Book, 2023 to 2030, Compiled Report By Grand View Research Pleated Membranes Market Report Highlights The global pleated membranes market size was reached to USD 12,313.5 million in 2022 registering a CAGR of 5.1% from 2023 to 2030, according to a new report by Grand View Research, Inc. • Pleated membranes are considered the most effective filtration membrane for use in a wide range of applications, including vaccine purification, the production of drinking water, and the sterilization of natural gas to remove unwanted particles from the solution. • These membranes are durable and can withstand harsh conditions, including high-temperature fluctuations, which reduces the requirement for maintenance and replacements. These factors are expected to increase the demand for pleated membranes in the coming years. • China and the U.S. have dominated the pleated membrane market and accounted for a combined revenue share of more than 34% in 2022. • Factors such as high industrial growth, infrastructure investments, and environmental regulations, growing spending on research and development (R&D) to enhance the performance and application of pleated membranes are considered the major growth drivers in these countries. Hollow Fiber Membranes Market Report Highlights The global hollow fiber membranes market size was reached to USD 876.1 million in 2022 registering a CAGR of 15.1% from 2023 to 2030, according to a new report by Grand View Research, Inc. • By membrane material, the polyethersulfone (PES) segment dominated the market with a revenue share of 35.7% in 2023 and is projected to exhibit the fastest CAGR during the assessment period. • By process, the reusable hollow fiber membranes segment dominated the market with a share of 53.5% in 2023. • By technology, the microfiltration segment held the largest revenue share of 52.4% in 2023. Microfiltration is a low-pressure technique for separating high-molecular-weight compounds from dissolved solids. • By end-use, pharmaceutical and biotechnology companies segment held the largest share of 44.5% in 2023. • North America dominated the regional market with a revenue share of 39.4% in 2023. During the projected period, the region is expected to retain its leadership. • In the future, the expansion of the market in the Asia Pacific region is anticipated to grow exponentially. Order your copy of Free Sample of “Filtration Membrane Industry Data Book –Market Size, Share, Trends Analysis And Segment Forecasts, 2023 - 2030” published by Grand View Research Competitive Landscape The major players are engaging in strategies such as high R&D investments to introduce membrane separation products with enhanced durability and higher flow rates. Manufacturers are developing application-based membrane filtration to address the specific requirements of the end-use industries. Some of the major manufacturers also have an extensive distribution network to connect with their customers across regions and gain a competitive advantage. Key players operating in the Filtration Membrane Industry are – • Synder Filtration, Inc. • Cole-Parmer Instrument Company, LLC • Berghof Membrane Technology GmbH (BMT) • ALFA LAVAL • DuPont • Pall Corporation • 3M • Donaldson Company, Inc. • TORAY INDUSTRIES, INC. • SPXFLOW • Kovalus Separation Solutions • MMS Membrane Systems • MANN+HUMMEL • Arvind KaiGo  Global air compressor sector database is a collection of market sizing information & forecasts, competitive benchmarking analyses, macro-environmental analyses, and regulatory & technological framework studies. Within the purview of the database, such information is systematically analyzed and provided in the form of outlook reports and summary presentations on individual areas of research. The growing adoption of variable-speed systems, low maintenance cost, effective operation, and retrofitting for existing systems are some factors propelling the demand for air compressors across key end-use industries. Energy-efficient compressors are witnessing a surge in demand owing to their cost-effective operations. However, the growing number of gas compressor stations has increased concerns about air quality. Hence, air monitoring systems are widely being installed for measuring the impact of air and gas compressors. Additionally, the subsequent introduction of non-oil and gas-based projects, and continuous investments in the industry, are driving the demand for air compressors. Access the Global Air Compressor Industry Data Book, 2023 to 2030, Compiled Report By Grand View Research Rotary/Screw Air Compressor Market Report Highlights The global rotary air compressor market size is anticipated to reach USD 11.44 billion in 2022, according to a new report by Grand View Research, Inc. The market is projected to grow at a CAGR of 4.4% from 2023 to 2030. • In terms of lubrication, the oil-free lubrication segment is anticipated to witness the fastest CAGR of 5.4% over the forecast period. Oil-free rotary air compressors are made to offer the highest-quality air in compliance with industry requirements while having the lowest lifespan costs. For instance, Atlas Copco provides ZT & ZR compressors for the pharmaceutical, food & beverage, automotive, textile, medical, power generation, battery, chemical, and automotive industries, all of which need high criteria for compressed air quality • Based on type, the portable segment is anticipated to witness the fastest CAGR of 4.9% over the forecast period. The most demanding portable compressor applications are catered by portable rotary compressors. The screw air end is built to last for many years in situations with a high-duty cycle. In addition, rotary portable air compressors are helpful for applications that require high cfm output in a compact design. These aforementioned factors are anticipated to augment the market demand • In terms of application, the manufacturing application segment held the largest revenue share of 37.4% in 2022. Air compressors with rotary motors survive a long time since there is little to no capacity loss. These compressors are made to power tools that produce more power than typical machinery. In addition, these are made to create a constant flow rate, making them perfect for a range of industrial uses, including small machine shops, the production of food & beverages, and the manufacture of automobiles, among others • Asia Pacific region led the market in 2022 with the largest revenue share of 37.2%. This growth can be attributed to increasing urbanization, a rise in energy consumption, and the presence of manufacturing facilities in the region. Furthermore, the region has a strong manufacturing base due to the presence of the largest manufacturing economies such as China, Japan, South Korea, and India • In November 2021, Vanair Manufacturing, Inc. launched the Air N Arc 300 system. The system is designed specifically to meet the challenge of fitting under the slide-out tray or on the body of a box truck. It is lighter and more compact than standard units at 7.5 inches shorter. The unit provides more efficient use of truck bed that reduces cost by combining various power sources into a single machine, including a rotary air compressor, battery charger, 300 AMP welder, 7 kW generator, and battery booster. Order your copy of Free Sample of “Air Compressor Industry Data Book –Market Size, Share, Trends Analysis And Segment Forecasts, 2023 - 2030” published by Grand View Research Reciprocating Air Compressor Market Report Highlights The global reciprocating air compressor market size is anticipated to reach USD 5.25 billion in 2022, according to a new report by Grand View Research, Inc. The market is anticipated to grow at a CAGR of 4.1% from 2023 to 2030. • In terms of technology, the single-acting technology segment is anticipated to witness a CAGR of 3.9% over the forecast period. These compressors are commonly used in small industrial settings, home workshops, and other environments where moderate air compression is needed. Further, due to the durability offered by reciprocating air compressors, this results in the machine having a significant product life • The double-acting technology segment led the market in 2022 with a market share of 59.4%. Double-acting compressors are better suited for applications that require a continuous supply of compressed air. They can handle higher duty cycles and provide a more consistent output of compressed air • In terms of lubrication, the oil-free lubrication segment is anticipated to witness the fastest CAGR of 5.1% over the forecast period. Oil-free reciprocating air compressors are essential in applications where the compressed air must be completely free of oil contamination • Based on type, the portable type segment is anticipated to witness the fastest CAGR of 4.5% over the forecast period. Portable reciprocating air compressors are widely used in construction & mining activities. They are also extensively used across various industrial applications, owing to their convenience in shipping the equipment • In terms of application, the manufacturing segment held a 39.1% revenue share in 2022. This can be attributed to the rapid industrialization in developing economies such as India, China, and Brazil, coupled with increasing demand for advanced and energy-efficient air compressors in the manufacturing sector Centrifugal Air Compressors Market Report Highlights The global centrifugal air compressor market size is anticipated to reach USD 7.66 billion in 2022, registering a CAGR of 5.3% from 2023 to 2030, according to a new report by Grand View Research, Inc. • Based on lubrication, the oil-filled lubrication segment dominated the market with a revenue share of 61.7% in 2022. Oil-filled air compressors are extensively used in commercial applications within the energy, manufacturing, and industrial sectors. They are known for their durability and their ability to operate with reduced noise levels when compared to oil-free compressors • Based on application, the manufacturing segment is expected to showcase lucrative growth with a CAGR of 5.0% over the forecast period. The expansion of this market can be attributed to the swift industrialization taking place in developing economies like India, China, and Brazil. This is further fueled by the rising need for advanced and energy-efficient air compressors within the manufacturing sector • The Asia Pacific region held a dominant revenue share of 37.2% in 2022. The growth is propelled by the increasing demand for air compressors across various applications, including food and beverage, manufacturing, home appliances, and the oil and gas industry. In addition, the market benefits from the presence of numerous compressor manufacturers in India and China. Moreover, the substantial industrial infrastructure for electronics and semiconductor manufacturing in China and Taiwan is poised to further stimulate market expansion Go through the table of content of Air Compressor Industry Data Book to get a better understanding of the Coverage & Scope of the study. Competitive Landscape The air compressor manufacturers adopt several strategies, including mergers & acquisitions, partnerships & joint ventures, new product developments, distributor agreements, new online channels, and geographical expansions, to augment their market presence and cater to the ever-changing consumer requirements. Key players operating in the Air Compressor Industry are – • Atlas Copco • Bauer Group • BelAire Compressors • Cook Compression • Compressor Products International (CPI) • Galaxy Auto Stationary Equipment Co. Ltd. • Gast Manufacturing, Inc. • GE Energy • Heyner • Hitachi Industrial Equipment Systems Co. Ltd. • Hoerbiger • Ingersoll Rand Plc • Kaeser Compressors • MAT Industries, LLC • FS Elliot Co., LLC • Hanwha Techwin • Sullair LLC • Sundyne • Kaeser Kompressoren SE • Doosan Portable Power • Sullivan-Palatek, Inc. • Elgi Compressors USA, Inc. • Zen Air Tech Pvt. Ltd. • Oasis Manufacturing • Frank Technologies Sheet Metal Industry To Rise Because It Is Versatile Material That Makes The World Go Round11/6/2023  Global sheet metal sector database is a collection of market sizing information & forecasts, trade data, pricing intelligence, competitive benchmarking analyses, macro-environmental analyses, and regulatory & technological framework studies. Within the purview of the database, such information is systematically analyzed and provided in the form of outlook reports (1 detailed sectoral outlook report) and summary presentations on individual areas of research along with a sheet metal statistics e-book. The automotive segment is anticipated to remain a key consumer of steel and aluminum sheets. Sheet metal components are used to manufacture numerous automotive parts such as body panels and tops, chassis, vehicle bumpers, fenders, hubcaps, moldings, trim pieces, engine and transmission components, brake components, windshield wiper arms, and system components. Access the Global Sheet Metal Industry Data Book, 2023 to 2030, Compiled Report By Grand View Research Steel Sheet Market Report Highlights The global steel sheet market size was valued at USD 177.02 billion in 2022 and is expected to expand at a compound annual growth rate (CAGR) of 2.6% from 2023 to 2030. • Steel sheet products offer benefits such as high strength & quality, economic benefits, recycling ability, and low maintenance cost. • Increasing demand for galvanized sheets in construction applications, such as awnings, balconies, ductwork, fences, industrial walkways, ladders, building frames, and handrails, is likely to fuel the growth of the market. • In the automotive industry, steel sheets are used in the production of hoods, fenders, roofing, spring housing, and seating applications. • Sheet metal products have a high requirement in electric vehicles owing to the ability to produce a high volume of complex and precise parts. A significant rise in the production of EVs is expected to provide a lucrative opportunity for the sheet metal market. The global sales of EVs are surging rapidly. The recorded sales in 2020, 2021, and 2022 are 3.2 million, 6.7 million, and 10.5 million, respectively. China accounted for over 58.0% of global EV sales in 2022, with more than 6 million units sold in the country. Aluminum Sheet Market Report Highlights The global aluminum sheet market size was valued at USD 38.70 billion in 2022 and is expected to expand at a compound annual growth rate (CAGR) of 3.5% from 2023 to 2030. • Sheet metal parts are used in aircraft engines, missile and defense components, aircraft panels, and various other high-precision equipment in these industries. • Aluminum is the preferred material for application in the aerospace industry owing to its lightweight, effective cost, and high-strength characteristics. • This is because the reduction in aircraft weight allows aviation companies to accommodate a large number of air passengers in their planes. • In terms of revenue, North America is projected to grow at a CAGR of 3.1% from 2023 to 2030. Investments in construction & infrastructure along with high volume production of vehicles are projected to act as growth factors for the region. • Growing focus on the reduction of carbon dioxide emissions and sustainability is projected to provide a boost to the demand for aluminum over the coming years. Order your copy of Free Sample of “Sheet Metal Industry Data Book –Market Size, Share, Trends Analysis And Segment Forecasts, 2023 - 2030” published by Grand View Research Competitive Landscape Some of the market players are highly integrated in the supply chain to reduce dependency on raw materials. For instance, the operations of Tata Steel include iron ore & coal mining, energy production, crude steel production, and manufacturing of downstream products such as sheets, platers, bars, wires, and coils. Similarly, producers in the aluminum industry are also engaged in the production of raw materials and finished products. Key players operating in the Sheet Metal Industry are – • JSW • Tata Bluescope Steel • Nippon Steel Corporation • POSCO • United States Steel • JFE Steel Corporation • Baosteel Group • Arconic • Alcoa Corporation • Hindalco Industries Limited • Kaiser Aluminum • Constellium • Aleris Corporation • Hulamin • Norsk Hydro Global construction fasteners sector database published by Grand View Research’s is a collection of market sizing information & forecasts, trade data, pricing intelligence, competitive benchmarking analyses, macro-environmental analyses, and regulatory & technological framework studies. Within the purview of the database, such information is systematically analyzed and provided in the form of outlook reports (1 detailed sectoral outlook report) and summary presentations on individual areas of research.

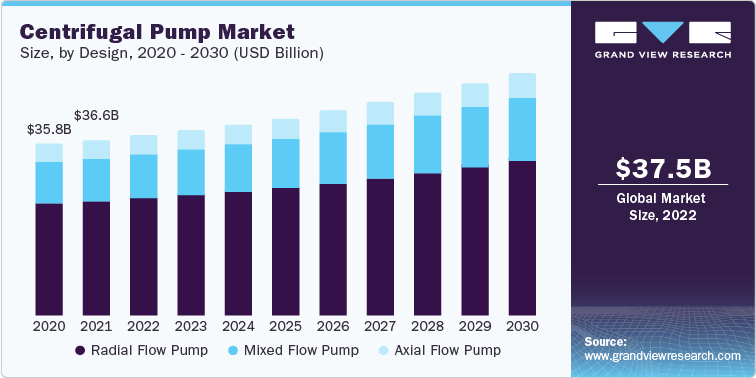

Access the Global Construction Fasteners Industry Data Book, 2023 to 2030, Compiled Report By Grand View Research Mechanical Anchors Market Report Highlights The global mechanical anchors market size is expected to reach USD 1.85 billion in 2022, registering a CAGR of 2.8% from 2023 to 2030, according to a new report by Grand View Research, Inc. • Stainless steel was the largest and fastest growing market segment and accounted for 54.2% of the revenue share in 2022 as stainless steel hardly gets oxidized when compared to other materials including iron, and carbon steel. Additionally, aesthetic shining appearance, corrosion resistance, low maintenance, and strength make stainless steel a widely used material for manufacturing mechanical anchors • Carbon steel accounted for USD 674.1 million for the year 2022 owing to its high strength. The presence of high carbon content makes them good at resisting abrasion and retaining shape under excess load in construction buildings. In addition, the material is primarily heat-treated by austenitizing, and quenching, followed by tempering to enhance its mechanical properties including yield and tensile strength • Residential applications accounted for a revenue share of over USD 476.0 million in 2022. The use of mechanical anchors in residential applications includes fixing wooden or plastic frames to the concrete or masonry units, railing and fences, and cable trenches. Metals such as aluminum and steel are widely used in the manufacturing of windows and doors in buildings owing to the lightweight and highly durable properties exhibited by the metals • Commercial applications accounted for 74.3% of the total market share for the year 2022. In commercial sectors, mechanical anchor finds its wide application in various malls, hotels, sports complexes, and industries. This building design is becoming more complex and is fitted with a wide variety of pipes, tubes, and cables suspended from the ceiling. These are primarily held on metal trenches which are fitted with mechanical anchors to fasten them to the underside of the concrete deck for support and hold • Companies are engaged in the adoption of strategic initiatives such as research & development and vertical integration to gain a competitive edge Bolts Market Report Highlights The global bolts market size is expected to reach USD 6.33 billion in 2022, progressing at a CAGR of 5.4% from 2023 to 2030, according to a new report by Grand View Research, Inc. • M8 was the largest product segment in 2018, in terms of revenue, and is expected to generate a revenue of USD 9.5 billion by 2028, on account of its wide application scope in industrial and construction segments • GR 8.8 segment is expected to progress at a CAGR of 4.8%, in terms of revenue, from 2020 to 2028, owing to its extensive use in railroad equipment, motors, processing equipment, and engines • North America market was valued at USD 9.4 billion in 2018 owing to the presence of notable aerospace and automotive manufacturing companies coupled with the revival of construction renovation sector • The bolts market is dominated by the presence of large players operating through multiple sales channels such as direct and distributor-based supply, which aids them in grabbing a high market share. Order your copy of Free Sample of “Construction Fasteners Industry Data Book –Market Size, Share, Trends Analysis And Segment Forecasts, 2023 - 2030” published by Grand View Research Chemical Anchors Market Report Highlights The global chemical anchors market size is expected to reach USD 0.95 billion in 2022, according to a new report by Grand View Research, Inc. It is expected to expand at a CAGR of 3.9% from 2023 to 2030. • By product, capsule adhesive anchors are expected to register the fastest CAGR of 5.0% over the forecast period owing to the increasing use of the product in the infrastructure and commercial segments • In terms of resin, unsaturated polyester chemical anchors are primarily used in masonry and uncracked concrete applications. However, methacrylates and pure epoxy type anchors are better suited for more demanding applications, including rebar and fractured concrete • The rising construction spending, particularly in the emerging economies, is a key factor promoting growth in the chemical anchor industry. Rising product awareness, coupled with the high consumer spending in the residential sector, is propelling the demand for chemical anchors • In the U.S., the demand for chemical anchors is expected to increase on account of the growing investments in infrastructure repair and rebuilding. Chemical anchors are being used in a majority of steel constructions, column bases, and scaffold anchoring • Manufacturers in the chemical anchor industry are involved in adopting several strategies, including acquisition, joint venture, new product development, and geographical expansion, which aid in enhancing their market penetration Nails Market Report Highlights The global nails market size is expected to reach USD 10.29 billion in 2022, registering a CAGR of 3.8% from 2023 to 2030, according to a new report by Grand View Research, Inc. • The stainless steel segment is expected to grow at a CAGR of 4.5% over the forecast period. Stainless steel is an expensive raw material, resulting in comparatively higher prices for end products such as nails. However, these nails offer a long-lasting solution with minimal maintenance requirements. Additionally, recycling stainless-steel nails is also considered to be an easy process. These factors are expected to fuel the global demand for stainless steel nails for usage in various construction projects • Concrete construction dominated the market and is further anticipated to grow at a CAGR of 4.7% over the forecast period. Concrete is the most common material used in construction projects. The material is made by mixing several other materials such as water, gravel, stones, cement, and aggregates. These materials together result in long-lasting building solutions. Furthermore, concrete is also highly preferred in the construction of sidewalks, garages, basements, driveways, columns, manholes, and beams on account of its superior strength • The Central & South America region is expected to grow at a CAGR of 3.3% over the forecast period. Emerging economies, such as Argentina, Brazil, and Peru are witnessing population growth coupled with rapid urbanization. These factors are triggering the construction of residential and commercial units in Central & South America, thereby fueling the product demand • The market for construction nails is highly competitive due to the presence of a large number of local players. Some of the key players include Simpson Strong-Tie, Grip-Rite, Shandong Oriental Cherry Hardware Group, Maze Nails, TITIBI, and Pan Chem Corporation Go through the table of content of Construction Fasteners Industry Data Book to get a better understanding of the Coverage & Scope of the study. Competitive Landscape The construction nails market is categorized as highly competitive owing to the presence of a number of large- and small-sized manufacturers of different types of these nails in their product portfolios. These players are focused on increasing their market share by adopting various strategies such as new product launches, research and development, mergers & acquisitions, and collaborations. Quality is a key factor for consumers, thus, the manufacturers are focusing on quality certification to gain consumer confidence. Key players operating in the Construction Fasteners Industry are – • Simpson Strong-Tie • Grip-Rite • Shandong Oriental Cherry Hardware Group • Maze Nails • TITIBI • Pan Chem Corporation • JE-IL WIRE PRODUCTION • Duchesne • BECK Fastener Group • DEACERO • Hilti Group • MKT Fastening • Power Fasteners • FIXDEX Fastening Technology • Illinois Tool Works Inc. • Sika AG • Würth Industrie Service GmbH & Co. KG • REYHER  Global centrifugal pump sector database is a collection of market sizing information & forecasts, trade data, pricing intelligence, competitive benchmarking analyses, macro-environmental analyses, and regulatory & technological framework studies. Within the purview of the database, such information is systematically analyzed and provided in the form of outlook report and summary presentations on individual areas of research. One of the key drivers behind this growth is the need for reliable and efficient fluid transportation in various applications. Centrifugal pumps offer advantages such as high flow rates, low maintenance requirements, and the ability to handle a varied range of fluids, making them indispensable in numerous industries. Furthermore, the development of advanced technologies, such as variable frequency drives (VFDs) and IoT-enabled monitoring systems, has enhanced the performance and efficiency of centrifugal pumps, further fueling their adoption. Access the Global Centrifugal Pump Industry Data Book, 2023 to 2030, Compiled Report By Grand View Research Radial Flow Pumps Market Report Highlights The global radial flow pump market size is anticipated to reach USD 24.4 billion in 2022, according to a new report by Grand View Research, Inc. The market is projected to grow at a CAGR of 3.6% from 2023 to 2030. • In terms of configuration, the single-stage radial flow pump segment held the largest revenue share of 62.8% in 2022 as this segment plays a crucial role in agricultural irrigation, helping to move water from water sources to fields and crops efficiently. • In terms of end-use, the oil and gas segment is anticipated to register a CAGR of 3.8% over the forecast period owing to its applications such as injection, hydraulic fracturing, crude oil transportation, and refining processes. The growth of the oil and gas industry contributes to the demand for radial flow pumps. • Several factors including industrialization, technical improvements, and growing urbanization have contributed to the remarkable rise in demand for energy fuel over the past few years, and North America is predicted to dominate the market over the projection period in terms of region. This is anticipated to increase the product's uptake by several businesses, including the water and wastewater treatment, power, and oil and gas sectors. • In May 2023, Xylem, Inc. launched a global pump manufacturing site in Egypt. Leading water brands including Flygt; Lowara; and Bell & Gossett will be manufactured and assembled at the new Xylem Egypt Plant, which will also produce parts and full units. The Xylem Egypt Plant will first produce Split-Case Centrifugal pumps for various uses, including irrigation, HVAC, and commercial building services, as well as End-Suction pumps for industry and irrigation. Mixed Flow Pumps Market Report Highlights The global mixed flow pump market size is anticipated to reach USD 9.1 billion in 2022, registering a CAGR of 4.7% from 2023 to 2030, according to a new report by Grand View Research, Inc.